Featured

Accenture’s AI Growth Story Faces Investor Skepticism as Shares Sink After FQ3 Earnings

Accenture plc (NYSE: ACN) reported solid FQ3/2026 financial results, including 6% revenue growth, a 9% increase in diluted earnings per share, and $3.6 billion in free cash flow. However, investors focused on reduced full-year revenue guidance, softer enterprise spending trends, and uncertainty around the timing of AI-related growth. Shares fell nearly 18% following the earnings release as the market weighed whether artificial intelligence can drive meaningful revenue acceleration. Accenture also announced major cybersecurity acquisitions, including Dragos, runZero, and NetRise, expanding its presence in operational technology security while increasing acquisition spending expectations for fiscal 2026.

Shares of Accenture plc (NYSE: ACN) dropped nearly 18% yesterday as investors grew skeptical of the company’s AI growth story following its FQ3/2026 earnings report on Thursday.

Investors were concerned with a more reserved outlook as Accenture reported solid fiscal third-quarter 2026 financial results.

The drop reflects the market’s growing doubts as to whether the consulting giant can deliver the growth that investors expected from the AI boom.

In FQ3/2026, the company’s revenue grew by 6% in U.S. dollars and 3% in local currency to reach $18.7 billion. The diluted earnings per share increased 9% to $3.80, the operating margin grew 20 basis points to 17.0%, and the free cash flow reached $3.6 billion. New bookings were $19.3 billion.

At first glance, it seemed good for a company of Accenture’s size. But investors seemed to ignore the quarterly results and instead focused on growth that may continue to be limited despite AI’s increasing adoption.

Guidance Cut Overshadows Earnings Beat

The market’s concern was that management lowered its full-year revenue growth guidance to 3% to 4%, from the previous range of 3% to 5%. Excluding the effect of its U.S. federal business, the company’s growth is now expected to be between 4% and 5%, compared to the previous range of 4% to 6%.

Weakness related to the Middle East and deferred client spending were cited as reasons for an approximately $100 million revenue shortfall relative to expectations. On the earnings call, CEO Julie Sweet said the company also saw slower decision-making and lower discretionary spending in parts of Europe and the Middle East.

Investors are concerned about geopolitical issues and lower enterprise spending patterns. While many large companies have been investing billions of dollars in AI infrastructure, they are still scrutinizing their consulting spend and big project costs.

Those concerns were confirmed in the company’s FQ4/2026 guidance. Revenue growth is within a relatively broad range of 1% to 5% in local currency, which management said was driven by continued uncertainty in client spending patterns.

The AI Opportunity is Real, but Questions Remain

Management reiterated during the earnings call that AI demand continues to grow. During the quarter, Accenture reported that another 100 clients launched new advanced AI projects and showcased several high-profile transformation programs with large global clients.

But investors are asking: if AI is such a big opportunity, why is the overall revenue growth in the low single digits?

Management stated that AI adoption is still in its early stages and that several clients have been laying the groundwork needed to support enterprise-scale AI deployments. In fact, before any meaningful AI applications can be deployed, projects such as cloud migration, cybersecurity upgrades, data modernization, and redesigning the operating model need to be completed.

Accenture remarked that approximately half of advanced AI projects generate broader data-related work.

Yet some investors may be concerned that AI is proving to be a double-edged sword for consulting firms. AI opens up new possibilities, but it can also automate parts of traditional consulting and outsourcing work.

During the call, management noted that just like in the early days of cloud computing, when businesses needed support with managing their cloud expenditure, companies are now looking for support for optimizing their AI infrastructure and token usage costs.

The challenge for Accenture is proving that AI is going to grow its revenue opportunity even more than it shrinks service delivery models.

Cybersecurity Acquisitions Raise Strategic and Financial Questions

Accenture also announced an agreement to acquire a majority stake in Dragos, along with the full acquisitions of runZero and NetRise.

The transactions were a big step into the operational technology (OT) security industry, which focuses on securing critical infrastructure like power grids, pipelines, manufacturing systems, and industrial facilities.

The strategic thinking is understandable. The role of AI in the physical infrastructure is growing more significant, and so is cybersecurity.

Management believes the deals will have a major impact on the company’s addressable market and accelerate its transition to software-based and recurring revenue models.

Several Risks Persist

The first is that the acquisition plan is large. Accenture now plans to spend around $9 billion on acquisitions in fiscal 2026, significantly more than previously thought.

Secondly, management said the acquired cybersecurity assets generate about $208 million in annual recurring revenue and are growing rapidly. However, the deals are unlikely to have a material impact on a company that is projected to generate about $74 billion in annual revenue this year.

Finally, investors may be wondering if Accenture can merge a number of software businesses together and maintain the same rate of growth and entrepreneurial spirit.

Investors Looking for Proof, Not Potential

Accenture remains one of the largest and most profitable consulting and technology firms. The company still generates solid cash flow, continues to expand margins, returns cash to shareholders, and wins big enterprise deals. The strengths were evident in the FQ3 results.

However, the market response is that investors expect to see more than evidence of operational execution. They’re looking for evidence that AI is a growth driver, rather than a growth enabler. They want to know they will get a return on billions of dollars in acquisition investments. They want greater visibility into when big-picture AI adoption will yield tangible revenue gains.

For now, Accenture’s financial results highlight a company going through a complicated transition. While AI and cybersecurity present significant opportunities, investors appear focused on the difference between that opportunity and the relatively low growth rate they actually have.

Yesterday’s share price tumble suggests that, for the time being, the market remains unconvinced.

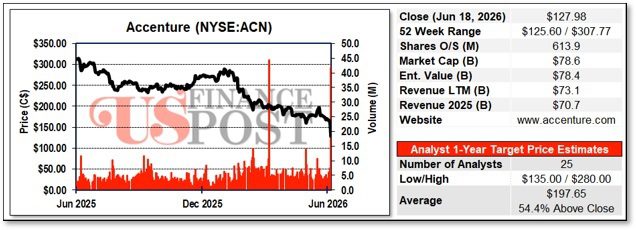

FIGURE 1: Accenture Stock Chart and Market Data

Source: S&P Capital IQ